Daily Market Outlook, February 4, 2020

Daily Market Outlook, February 4, 2020

The Asian equity market has rebounded strongly overnight despite further reports of Coronavirus cases, including the first death in Hong Kong, as the PBOC slashed its reverse repo rate by 10bps in its latest move to address the virus fallout in addition to liquidity injection announced yesterday.

The Australian central bank as expected, left interest rates unchanged. However, it noted downside risks to economic growth and said that it stood ready to lower rates if necessary.

In the US, the results from the Iowa caucus have been delayed after officials found “inconsistencies”. This is the opening event of the process to choose the Democratic candidate for November’s Presidential election.

Major US indexes rose 0.5- 1.3%, tracking higher European equities, US treasuries yields recovered by 1-4bps along the curve as risk sentiment improved; 10Y UST yield picked up 2bps to 1.53%.

Gold retreated by nearly 0.8% to $1576.73/ounce while crude oils suffered from major losses on virus concerns despite news that Saudi Arabia was pushing for production cuts; global benchmark Brent crude plunged by a whopping 6.4% overnight, its biggest drop since mid-September last year.

US ISM PMI returned to expansion: The ISM Manufacturing Index beat expectations at 50.9 in January (Dec: 47.8), marking its first above 50 reading in six months to indicate an expansion in manufacturing activity at the start of the new year. The upturn in PMI reflects rebounds in new orders, productions, new exports orders, imports as well as higher prices. ISM said that comments from respondents were generally positive but added that “global trade remains a cross-industry” but many were positive for the first time in many months. Meanwhile, the separate IHS Markit PMI ticked lower to 51.9 in January (Dec: 52.4) to suggest slower growth in overall manufacturing conditions, dragged down by a “renewed drop in exports orders”, yet business sentiment picked up to 7-month high.

US construction spending slipped at year end: On a less positive note, construction spending dropped 0.2% MOM in December (Nov: +0.7% revised) versus analysts’ forecast of 0.5% gain. Breakdown shows that spending on residential projects rose by a steadier 1.4% MOM (Nov:+1.5%), in line with a gradually recovering housing market whereas spending on commercial projects dropped for the first time in six months by 1.2% MOM (Nov: +0.2%). The newly revised November figure nonetheless suggests an upward revision to 4Q GDP growth which had come in at 2.1% QOQ in the advance reading. Compared to 2018, total 2019 spending dropped by 0.3% to $1.3 trillion (2018: +3.3%).

Eurozone manufacturing downturn continued in January: The IHS Markit Eurozone Manufacturing PMI rose to 47.9 in January (Dec: 46.3), confirming that operating conditions in the euro area manufacturing sector continued to weaken at the start of the year. Germany again was the weakest performing country reflecting its struggling auto industry that is simultaneously facing transition and weaker global demand.

UK manufacturing PMI at neutral 50: The IHS Markit/CIPS Markit PMI jumped to 50.0 in January (Dec: 47.5) as the manufacturing sector bounced back from eight months of downturn at the start of the year, thanks to reduced political uncertainties just ahead of Brexit day on 31 January. The survey reported that signs of stabilization are showing in hiring and business confidence while new exports remain weak.

Japan manufacturing PMI indicates still-weak manufacturing industry: The headline Jibun Bank Manufacturing PMI rose a little to 48.4 in January (Dec: 48.8) to mark its ninth consecutive month of sub-50 reading. The negligible rise in PMI suggests that Japanese manufacturers continued to face a challenging start to the year as demand condition remains fragile.

At 2am GMT President Trump will give his annual State of the Union address. With only nine months until November’s poll the President can be expected to make the case for his reelection. So the address is likely to paint a very positive picture of the economy and may also promise further fiscal stimulus measures including tax cuts. There will also be interest for markets in what the President has to say on foreign policy including trade relations with the EU

Today’s Options Expiries for 10AM New York Cut (notable size in bold)

- EURUSD: 1.1030 (EUR658mn); 1.1040 (EUR396mn); 1.1050 (EUR331mn); 1.1150 (EUR647mn)

- GBPUSD: 1.3000 (GBP248mn)

- USDJPY: 108.00 (USD570mn); 108.15 (USD390mn); 108.35 (USD340mn); 109.00 (USD1.1bn); 109.50 (USD351mn)

- AUDUSD: 0.6765 (AUD1.2bn); 0.6800 (AUD1.2bn); 0.6825 (AUD1.8bn)

Technical & Trade Views

EURUSD (Intraday bias: Bullish above 1.1050)

EURUSD From a technical and trading perspective, the spike through 1.1050 was satisfied by bids below as yesterday's lows support look for a test of offers and stops above 1.11. A breach of 1.1030 would suggest a false upside break and a retest of bids and stops below 1.10

GBPUSD (Intraday bias: Bearish below 1.3060)

GBPUSD From a technical and trading perspective, the failure below 1.31 confirmed another false upside break and return to test range support below 1.30 as 1.3060 act as resistance look for a test of the yearly pivot towards 1.29

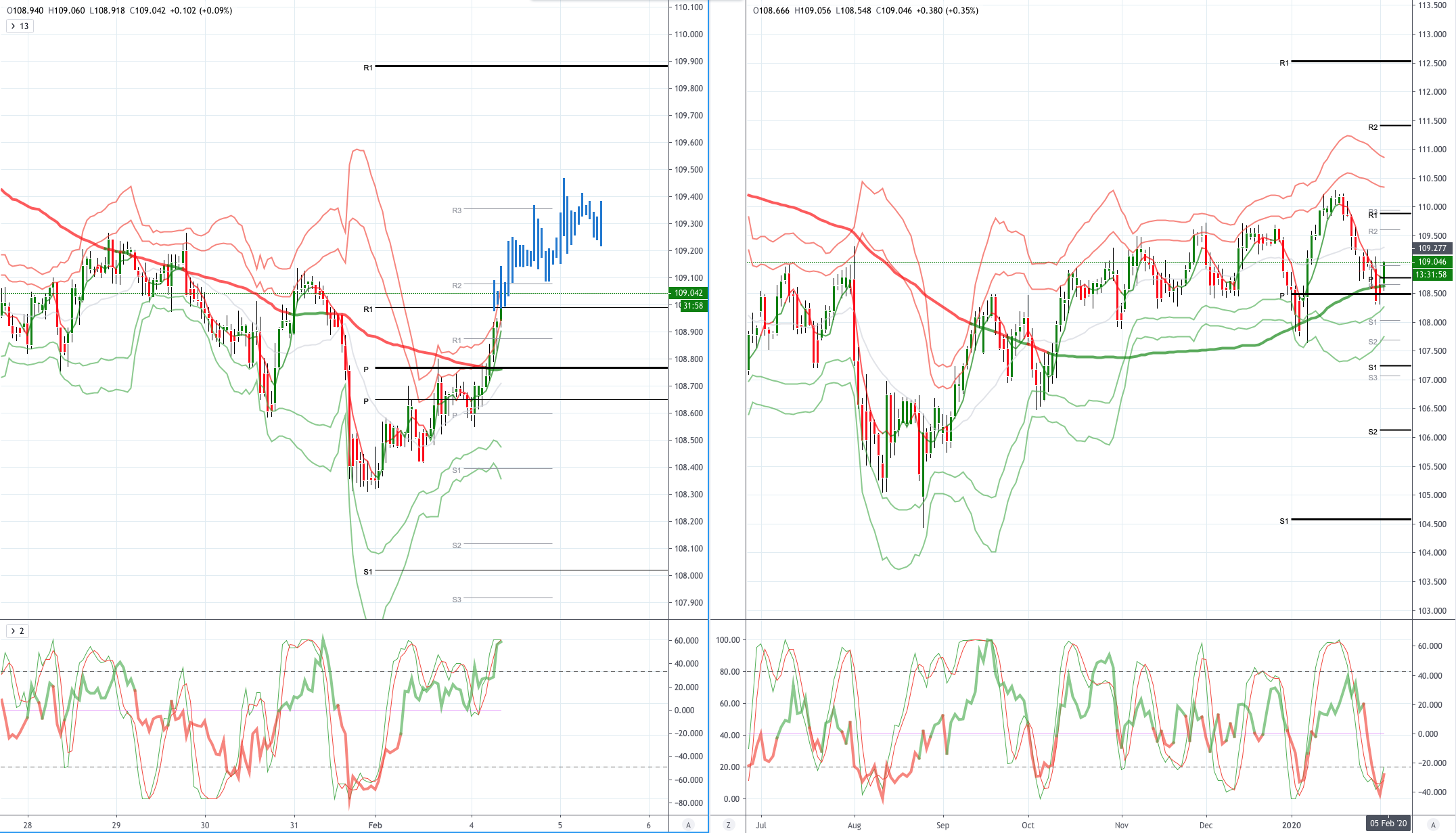

USDJPY (intraday bias: Bullish above 108.60)

USDJPY From a technical and trading perspective, the day only a close back through 108.80 suggests a reversal in sentiment and target a retest of 109.50 offers and stops

AUDUSD (Intraday bias: Bullish above .6720 Bearish below)

AUDUSD From a technical and trading perspective, .6680 yearly first support pivot point attracts bids overnight, a daily close above .6720 will flip the daily charts bullish and open a test of offers towards .6800 and stops above

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 73% and 70% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!