Dovish Fed, “Meme” Stocks’ Parabolic Surge Could Lead to Decline in Fragile US Market

The Fed confirmed yesterday that it will continue to flood the US banking sector with liquidity, at least at the current pace; limiting appreciation of market interest rates, including government bond yields. The Fed will continue to make monthly purchases of Treasuries and MBS in the size of $120 billion per month. According to the Fed, recovery of the economy continued to moderate and risks of early rate hikes outweigh risks of being late with policy tightening.

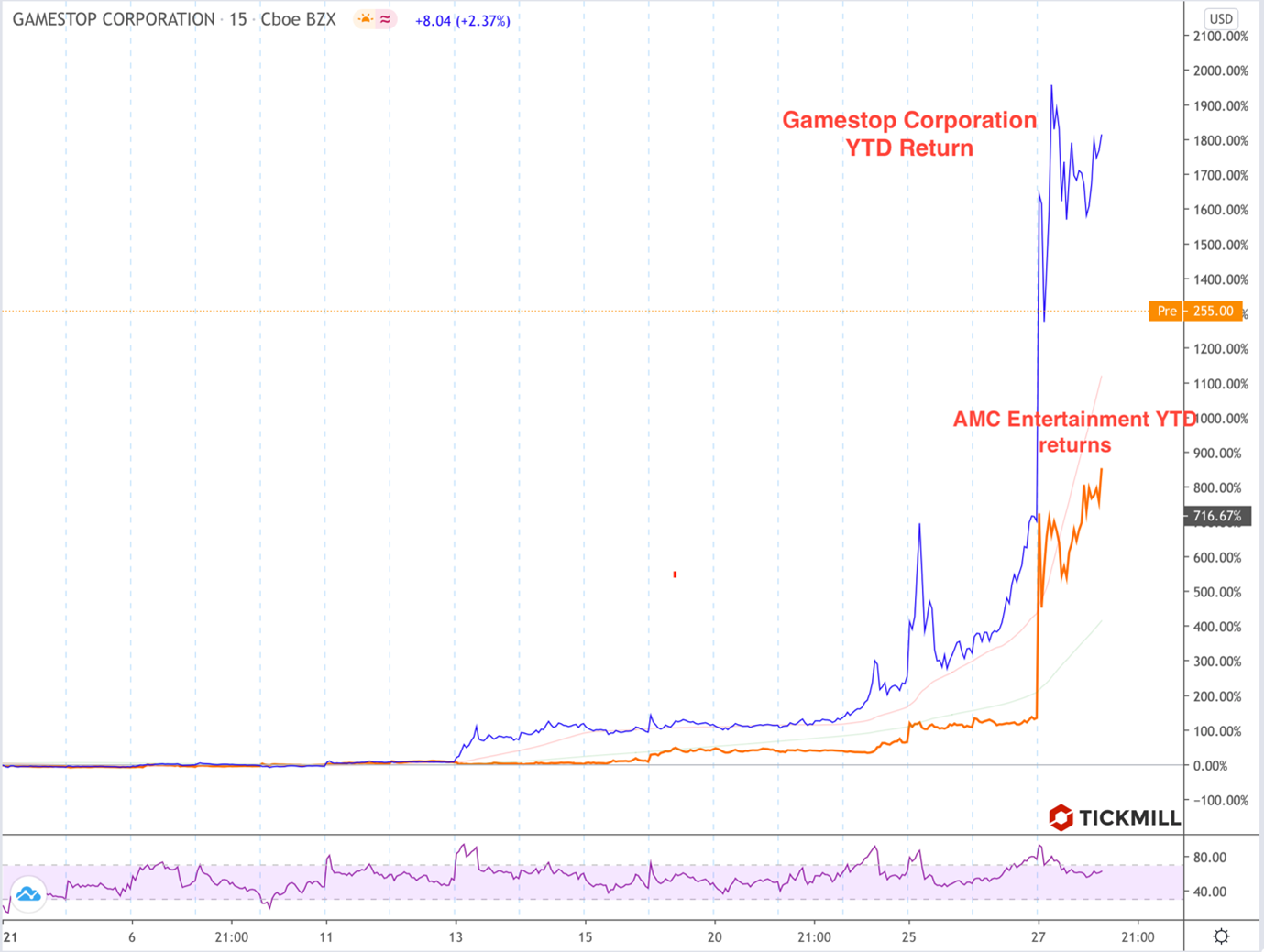

Fed’s dovish update followed an outbreak of anxiety in the stock market where several hedge funds suffering from losses on their short selling positions (in particular, on “meme” stocks such as GME or AMC, posting 2000% and 860% YTD gain thanks to immense interest from retail investors) triggered a wave of forced liquidations that spilled over to the broader market with fragility near historical highs contributing to the decline:

The SEC's announcement that they are closely monitoring market volatility and restriction of trading by US brokers on some stocks and options due to increased risks increased investors’ worries about US bubbles, discouraging them to buy dips.

Worsening near-term economic outlook sent 10-year Treasury yield to 1%, the lowest level in 3 weeks:

Recall that just a week and a half ago, YTM on 10-Yr T-Note was at 1.18% amid expectations that the concentration of power in the hands of the Democrats will entail the approval of hefty government stimulus package with the size of $2 tn. However, subsequent comments from several members of Congress, in particular the head of the Democrats in Congress Chuck Schumer, led to a sharp shift in expectations in favor of austerity in expected government spending, with new stimulus package being twice as less as expected. In this situation, markets have become more susceptible to macroeconomic news in the US and Europe, which deterioration were marked with the release of January NFP report, indicating that the US economy started to lose jobs in December.

Tuesday release of one of the key consumer reports - orders for durable goods (expensive goods consumed for more than 6 months) did not live up to expectations, adding negative news to the story of slowdown in the US economic recovery. Orders rose 0.2% versus 0.9% forecast.

The confluence of the circumstances described above led to the fact that investors holding stocks at peaks lost patience. Downside momentum is gaining traction today, European markets erased from 0.5% to 2%, US stock index futures indicate that Tuesday pullback in US markets by more than 2% will likely extend into today NY session with near-target at SPX at 3700 points.

Today, market dynamics can be sensitive to the data on US GDP for 4Q of 2020, which is expected to show economic growth of 4% YoY. A reading below forecast could boost sell-off in the market with rapidly growing fragility.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% and 65% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.