Gold Breaks Out of Key Bullish Channel as Fed Signals Policy Tightening Will Likely Continue

The two-week consolidation period of gold price around $1950 has ended with a breakdown below the lower bound of the main ascending channel:

The risk is increasing that sellers will temporarily seize the initiative, as buyers have lost their main stronghold in the form of the ascending corridor that started back in October 2022. From my perspective, buying interest is likely to emerge closer to $1900 per troy ounce.

The fundamental background for gold has also undergone a significant change (at least until new data on the US is released), as the FOMC dismissed expectations of a rate cut in late 2023. Despite taking a timeout, the central bank made every effort to convince the market not to draw conclusions about the end of tightening. Powell made it quite clear (almost openly) that all FOMC members agreed that it would be appropriate to continue raising rates and that rate cuts in 2023 should not be expected. Furthermore, the Fed chairman believes that there hasn't been much success in reducing core inflation, and in order to expect easing, a "decisive" downward movement in Core PCE needs to be seen. The chart below indeed shows that the core growth rate of consumer prices has been "stuck" in the range of 4.6-4.7% since November 2022:

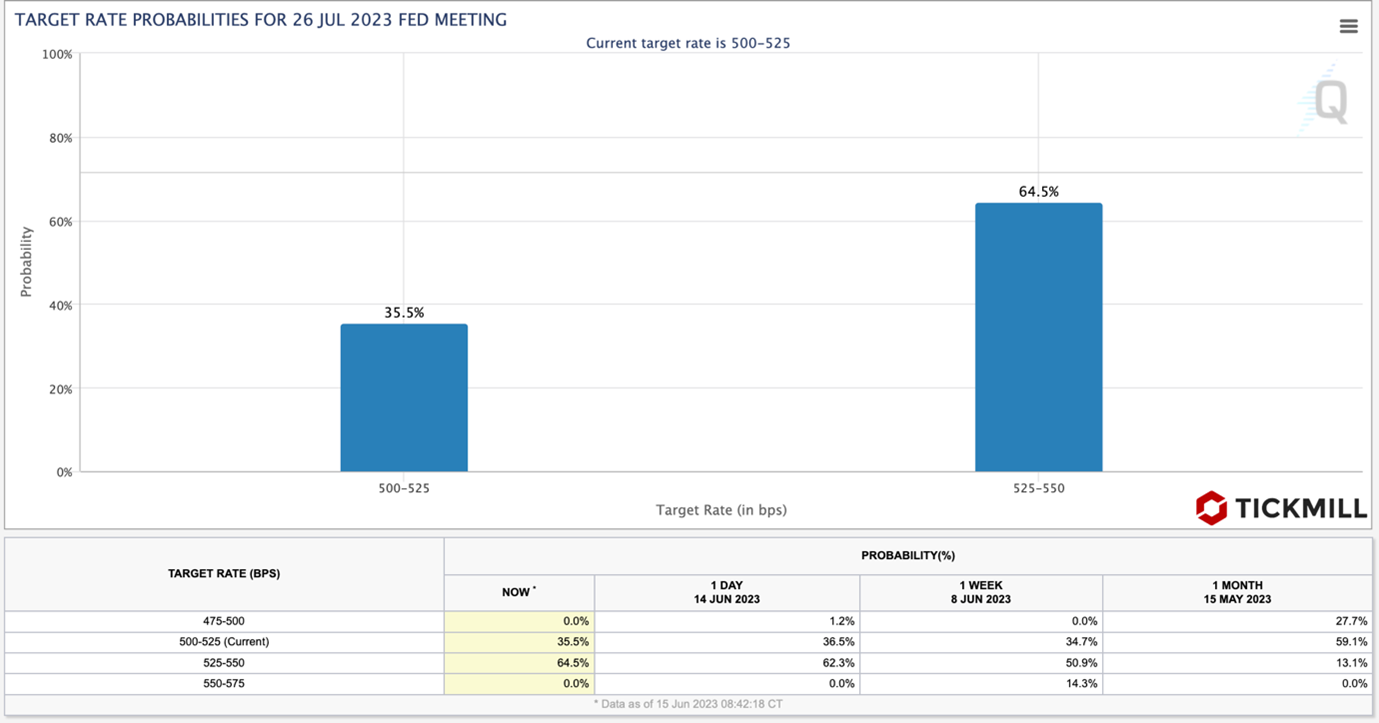

Of course, the central bank should avoid making "promises" about future decisions, as they would lose their effectiveness. Therefore, Powell tried to maintain uncertainty regarding the July decision by stating that although July was discussed, no decision has been made on it. In addition, he clearly stated that the term "skip" (one meeting) is incorrect (if it were correct, it would automatically mean that tightening would definitely resume in July). Nonetheless, the market increased the chances of tightening in July from 55% to 64%:

Regarding incoming data, retail sales in the US in May turned out to be better than expected, with a monthly increase of 0.3% compared to a forecast of 0.1%. Initial jobless claims remained at the same level of 262,000 (forecast: 249,000). Import and export price inflation was lower than expected, and previous figures were also revised downward. The dollar tumbled along with bond yields, despite the positive surprise in consumption. It is likely that inflation data has become more significant in assessing the prospects of July tightening.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.