Institutional Insights: Credit Agricole FX Weekly 9/1/2026

FX Weekly — Fire Caracas

US President Donald Trump kicked off the year with a surprise intervention in Venezuela. Markets have largely looked through the geopolitical headline risk, and oil is only modestly higher. Venezuela may hold the world’s largest crude reserves, but extracting and exporting meaningful volumes requires heavy investment—something the current political backdrop and low oil prices don’t encourage. As a result, it’s still questionable whether Venezuela can drive a material increase in global supply that would structurally push oil lower. Oil traders are also watching Iran, which remains a parallel risk channel.

Oil → FX: who wins, who loses

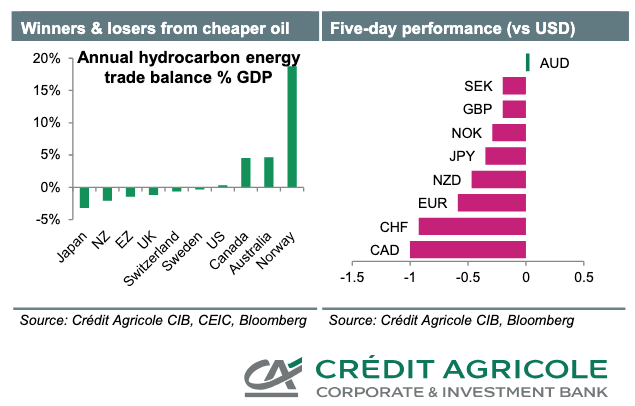

In pure terms-of-trade terms, lower oil prices would generally be:

Negative for: NOK, AUD, CAD, USD

Positive for: JPY, NZD, EUR, GBP, CHF, SEK

That said, Venezuela can’t be viewed through the oil lens alone.

AUD and CAD: oil isn’t the whole story

AUD has outperformed in early 2026, supported by rising expectations for RBA hikes and record-high copper prices.

CAD has lagged. The US “purchase” of 30–50 million barrels of sanctioned Venezuelan heavy crude is only about 1–2 weeks of Canada’s heavy crude exports to the US, so it’s not a near-term game changer by itself.

The bigger issue is medium-term competition: Venezuelan barrels add downside risk to Canada’s export outlook—on top of the uncertainty from USMCA renegotiation risk during 2026.

EUR: underperformance and a slow grind lower

The EUR has also underperformed. Trump’s foreign-policy posture has weakened the West’s leverage over Russia, potentially prolonging the Ukraine war and adding strain to EU–US relations. Separately, US rhetoric around “acquiring” Greenland adds another layer of friction.

Bottom line: the base case remains a slow grind lower in EUR/USD. Lower oil prices could help the Eurozone at the margin by improving energy costs and competitiveness after the loss of cheap Russian gas. Cheaper energy also reduces Russia’s revenue base, increasing pressure on President Vladimir Putin to consider a peace deal.

USD: safe-haven bid + rates repricing risk

The USD is benefiting from safe-haven demand while US macro signals remain mixed. The bigger point is positioning: markets still look too aggressively priced for additional Fed cuts, and any unwind of that pricing should support USD outperformance.

Key catalysts:

US Non-Farm Payrolls (today)

US inflation + retail sales (next week)

Fed communication (Fedspeak)

Clarity on Trump’s pick for Fed Chair

US Supreme Court rulings on IEEPA tariffs and on whether Trump can remove Fed Governor Lisa Cook in the coming week(s)

Elsewhere, GBP will be driven by incoming UK data and BoE speeches.

FX & Gold Outlook

This outlook keeps a USD-supportive bias into 2026 while treating most G10 moves as a function of rates, growth differentials, and political/fiscal risk. The core message: several “known positives” in Europe are already priced, while USD downside narratives haven’t convincingly delivered.

---

🇪🇺 EUR/USD — Bearish bias through 2026

EUR/USD remains a sell-on-strength view from current levels. A lot of the bullish EUR story—ECB narrative and European fiscal support—looks reflected in price, while the usual USD negatives around US growth and the Fed are also well known.

### What could challenge the bearish EUR/USD view (near term)

- Political pressure on Fed independence (headline risk)

- More persistent US data softness linked to the recent government shutdown

### Why the base case still points lower

- The “sell America” theme hasn’t materialised: foreign inflows into US assets have stayed strong, reducing stress around US external balances.

- Ongoing political risk in France is a headwind for EUR, particularly into H1 2026.

- Net: EUR may struggle to outperform USD sustainably, keeping the bias toward renewed EUR/USD weakness through 2026.

---

🇺🇸 USD — Rebound risk as the market’s dovish Fed pricing unwinds

The USD has held up partly because fears of major capital flight from US stocks/bonds and reserve-currency erosion have faded.

### What still weighs on USD (near term)

- Concerns about the US economic trajectory

- “Fiscal dominance” fears shaping Fed expectations

### Why USD can firm over the next 6–12 months

- If US growth stabilises and inflation stays sticky, the market’s dovish Fed path can reprice.

- That repricing supports USD via rate differentials and reduces demand for short-USD hedges.

- “US exceptionalism” remains a live theme, reinforced by persistent foreign portfolio inflows and potentially fresh FDI in 2026.

- Structural point: the USD remains the dominant reserve currency, and credible alternatives are limited.

---

🇨🇭 CHF — Gradual depreciation, but not a collapse

After reaching decade highs vs EUR and USD, CHF has cooled heading into 2026. The base case is for slow, controlled CHF depreciation, as it increasingly acts as a funding currency if global risk conditions remain broadly stable. Low Swiss inflation and steady (if uninspiring) growth should limit downside.

---

🇯🇵 JPY — Politically capped, but still the best stagflation hedge

The expectation is for Japan’s current leadership (PM Sanae Takaichi) to lean against BOJ tightening, weighing on JPY via:

1. Slower BOJ normalisation

2. More fiscal spending supporting domestic risk assets (Nikkei)

3. Fiscal concerns resurfacing through higher spending

However, inflation is politically sensitive in Japan—especially if driven by a weak JPY—so there are limits to how far policy can suppress rate hikes.

### Key level framing

- BOJ “comfort zone” for USD/JPY: 145–155

- A sustained move above 155 increases the probability of faster BOJ normalisation

Net: JPY may face policy drag, but it remains the cleanest hedge if US stagflation risk rises.

---

🇬🇧 GBP — Constructive vs EUR (3–6 months)

GBP is viewed positively against EUR from here, supported by:

- Reduced fear of UK fiscal austerity after the autumn statement

- Easing UK stagflation risk, giving BoE more flexibility to support growth

- A sense that many GBP negatives are already priced

- Improved perceptions of UK sovereign creditworthiness via fiscal framing

Even if the BoE cuts, the rates market may be too dovish, which can help GBP outperform. Expectation: GBP can regain ground vs EUR over 3–6 months.

---

🇨🇦 USD/CAD — Gradual retracement lower

USD/CAD has broken an uptrend channel that held through much of H2 2025, helped by stronger Canadian data. The pair has tracked rate differentials closely and could continue doing so, with a gradual move toward 1.35 possible. The main risk is headline noise around the USMCA review.

---

🇦🇺 AUD — Grinding higher, with China/USD as constraints

AUD/USD is expected to trend higher through 2026 on:

- Relative resilience to US tariffs

- Firmer risk sentiment

- Rising expectations for RBA hikes

Caps on upside:

- Weak China growth

- A firmer USD backdrop

- Australia’s low productivity growth

---

🇳🇿 NZD — Slow upside grind, but not a straight line

NZD/USD is also seen edging higher into 2026, supported by:

- Improving NZ growth prospects

- Increasing odds of RBNZ hikes

- Firmer soft-commodity pricing

- Less extreme US equity outperformance vs Asia

Constraints remain similar: stronger USD and soft China growth.

---

🇳🇴 NOK — Fundamentally supported if risk stays calm

NOK has recovered from repeated setbacks, but Norway’s fundamentals and rate appeal suggest long-run appreciation potential, assuming no major global risk event disrupts sentiment.

---

🇸🇪 SEK — Needs macro proof to extend gains

SEK surprised as a top G10 performer in 2025, benefiting from its high-beta, EUR-proxy behaviour. For further gains in 2026, markets likely need clearer evidence Sweden can outperform the Eurozone, while the Riksbank’s FX reserves hedging programme may limit upside.

---

🟨 Gold (XAU) — Supported by debt + sticky inflation themes

Gold should remain supported by concerns that rising government borrowing and sticky G10 inflation make it difficult to find buyers for expanding public debt. If fiscal dominance fears weigh on real yields, that’s another tailwind for XAU.

### What would weaken gold in 2026

A clear rebound in US growth alongside higher real yields/real rates would be the main ingredient to meaningfully dent gold’s strength.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!