Institutional Insights - Credit Agricole USD: the Harris vs Trump trade

Institutional Insights - Credit Agricole USD: the Harris vs Trump trade

The USD October rally continues and some of the currency’s recent

gains reflect Donald Trump’s recovery in the polls ahead of the 5

November US presidential election. That being said, the race for the

White House remains very close and its outcome difficult to predict.

Recent client meetings have further suggested that the political

uncertainty may have forced FX investors to keep their market exposure

light. Our FX corporate clients have also signalled they have been front-

loading their hedging programmes and switching to hedging via FX

forwards for the same reason.

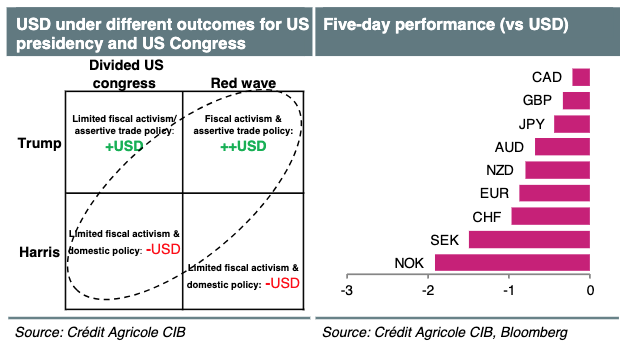

In particular, FX investors have been focusing on two equally-likely

outcomes from the US elections: (1) President Kamala Harris with a

divided US Congress that could result in a dysfunctional government but

leave the US fiscal policy stance and economic outlook little changed; or

(2) President Donald Trump and a ‘red wave’ in the US Congress that

could lead to extra fiscal spending and trade tariffs, in a boost to US

inflation and thus to the view that the Fed stance could be less dovish

than expected.

The above suggests that the risk-reward ahead of the vote could be for

muted downside but aggressive upside for the USD. A Harris victory

could be seen as confirming the status quo and weighing on the USD at

first, as Trump hedges are unwound. A US soft landing could soon boost

the appeal of the USD-assets, however. A Trump victory could result in

a stronger USD due to expectations of stickier inflation and a less dovish

Fed as well as growing macro and geopolitical risks. We also note that

Asian currencies bore the brunt of the USD rally after Trump won in 2016.

The data calendar is relatively light next week so FX investors will

continue to closely follow the polls ahead of the US election. Evidence

that Trump’s rebound in the polls has continued could see the USD

regaining more ground. Elsewhere, focus would be on the global

preliminary PMIs for October as well as a number of Fed, ECB, BoE and

BoJ speakers at the annual IMF and World Bank meetings in Washington

DC. North of the border, the BoC looks poised to speed up its easing

cycle with the delivery of its own 50bp cut in October, following a steeper

inflation undershoot last month.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!