Institutional insights: Goldman Sachs Trading Desk First Take On Tariffs

.jpeg)

WORSE THAN EXPECTED

FICC and Equities

Our desk is currently observing significant long selling in tech stocks and aggressive hedge fund (HF) shorting in macro products. S&P 500 futures have just reopened, trading down approximately 3%.

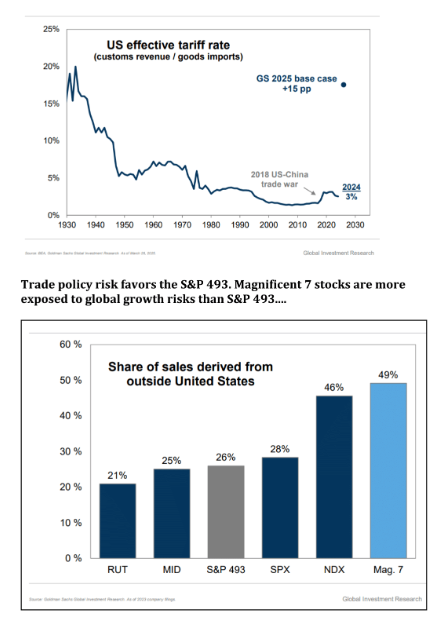

The bottom line: consistent derisking by both asset managers and hedge funds was evident in the lead-up to this event over the past two weeks. However, this afternoon’s announcement turned out to be worse than anticipated. Based on our analysis, the effective US tariff rate is likely closer to 20%, compared to our baseline assumption of 15%.

This is not good news. The higher tariffs will weigh on GDP growth, drive inflation upward, and maintain pressure on the US stock market. Uncertainty remains unresolved. With the current information, tomorrow looks set to be a very challenging day for the US stock market, potentially resembling an S&P 500 decline of around 4%.

At 4:10 PM, the Wall Street Journal (WSJ) published a headline that briefly excited the market (S&P Futures spiked to 5755 at 4:15 PM). However, by the time of writing, futures have dropped to 5515. The headline read: U.S. to Impose 10% Across-the-Board Tariff on All Imports, President Trump Says.

The initial optimism quickly faded as President Trump clarified that the 10% baseline tariff would take effect at midnight on April 5, with significantly higher reciprocal rates set to begin on April 9. Reuters released a detailed list of these reciprocal tariffs:

- China: Cumulative tariffs will reach 54% (34% + 20%).

- Canada and Mexico: Existing fentanyl/migration-related IEEPA orders remain unchanged. USMCA-compliant goods will continue to face a 0% tariff. Non-USMCA-compliant goods will incur a 25% tariff, while non-USMCA-compliant energy and potash will see a 10% tariff.

In summary, these developments are likely to exacerbate market volatility and economic uncertainty.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!