S&P500 Poised to Break 3900 on NFP Release as the US Recovery Gains Steam

TheDecember Non-Farm Payrolls report made investors seriously worried about impactof the coronavirus restrictions imposed in the winter on the US economy. Thenthe number of jobs in the economy shrank by 140 thousand, in particular due tothe fact that 372 thousand restaurant workers lost their jobs. That quicklychanged, though, with economic data for January pointing to expansion on allfronts. What kind of data made it possible to revise so quickly the outlook forthe US economy in the first quarter and what impact on stocks we should expect?

First,these are indicators of activity and employment in the services sector, whichaccounts for about 70% of US GDP. The sector was hit hard in November andDecember due to tightening of social distancing measures and forced businessclosures. This week, the data such as the ISM Service Sector Activity Index, ADPJanuary report, came out well above expectations. In particular, the ISMemployment sub-index rose from a depressed 48.7 points to 55.2 points,indicating quite fast recovery in the pace of hiring. The ISM report onmanufacturing sector released earlier this week also pointed to rebound inlabor demand - the corresponding sub-index ticked higher, from 51.7 to 52.6points. The 50-point mark in PMI indices separates zones of depression andrecovery.

TheADP estimate of job growth nearly tripled expectations of 174,000 versus 49,000forecast, although investors expected a rather downside surprise.

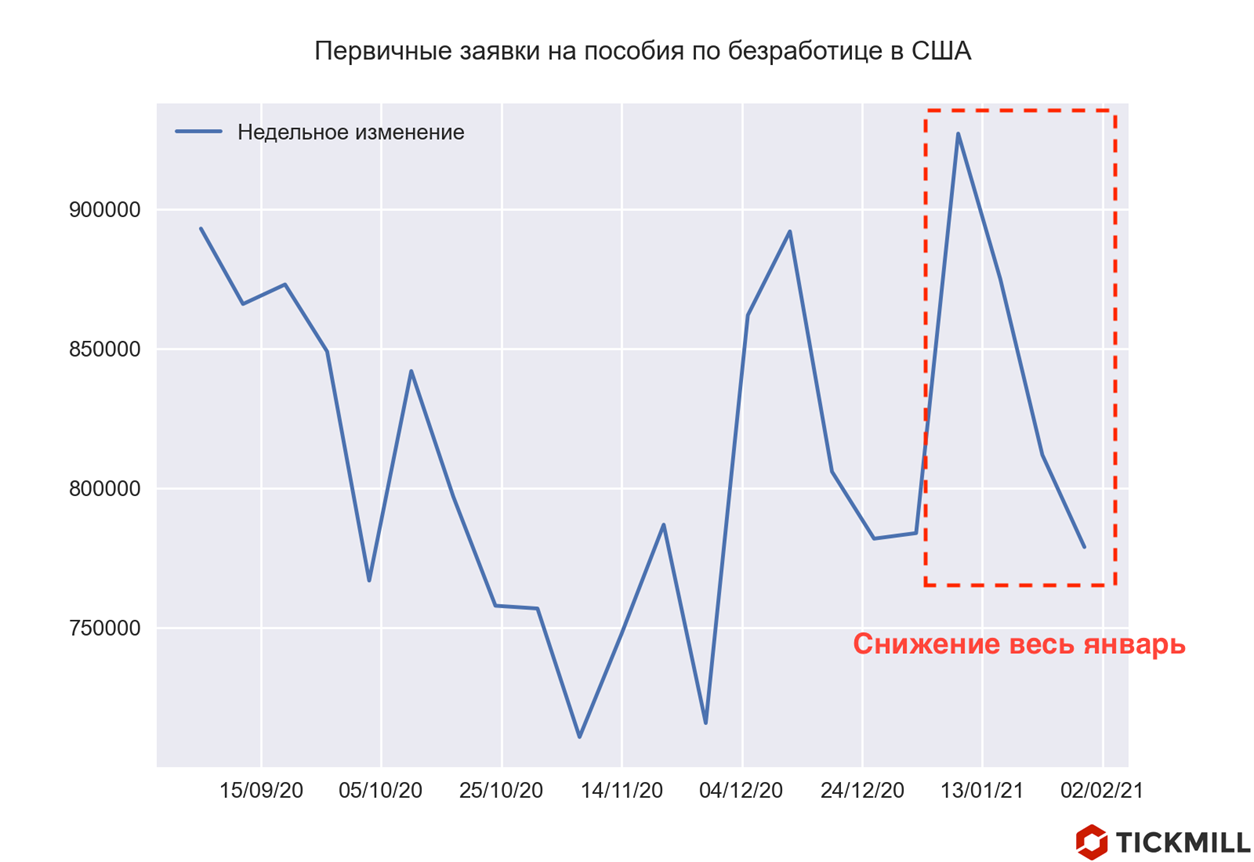

Thelatest readings in unemployment claims data, which experienced a brief surge inDecember, indicated that situation stabilizes with layoffs slowing quickly:

The growth of initial unemployment claims has been slowing for three weeks in a row while continuing claims also consistently beat expectations, dropping below 5 mn.

Following the data updates, Goldman updated its forecast for NFP jobs count, increasing its estimate from 125 to 200 thousand, which is higher than market consensus (50 thousand).

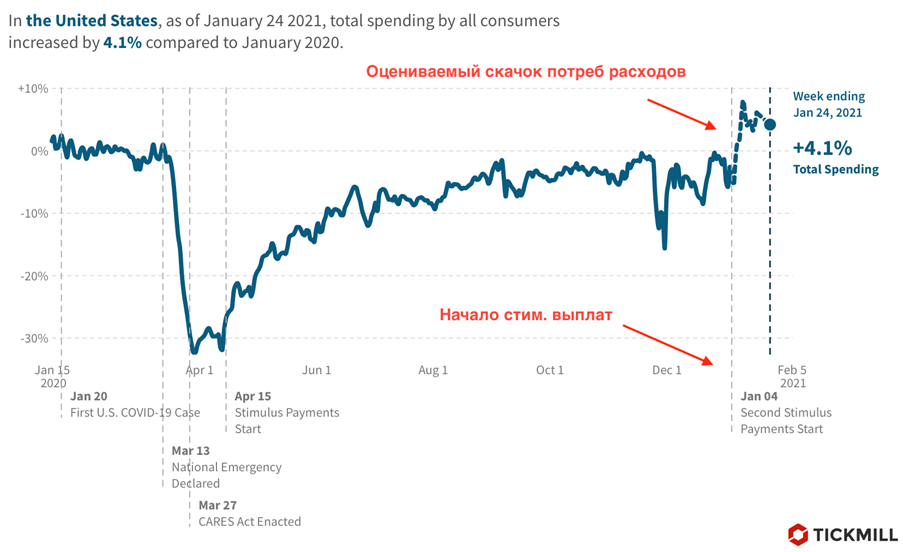

Second, in early January, stimulus checks from the government, which Congress approved in December, started to prop-up consumption. This led to high-frequency US consumption data indicating a spike in consumer spending in January:

High-frequency indicators indicate that in January, US consumption not only recovered, but could exceed pre-crisis levels by 4.1%. It’s extremely welcomed data as rising spending translates into rising firm revenues and consequent higher demand for labor.

The US dollar tends to appreciate either during downturns which are accompanied by tightening financial conditions => lack of liquidity (which drives demand for financing currencies, i.e. USD), or when there are expectations that US economy will outperform the Old World like EU or UK. The latest data on the US economy speaks in favor of the second scenario.

As we discussed in the article about possible new all-time highs in SPX, rapidly improving outlook for the US economy is accompanied by capital inflows in risk assets nominated in the US Dollar, and emerging economies, primarily in stock markets. The SPX hit its all-time high yesterday closing at 3875 points. In my opinion, a positive deviation in today's NFP report will be a catalyst for SPX breakout of 3900 mark. Preliminary data allow us to count on this outcome.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% and 65% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.