The Odds of a Dovish Fed in February Increase, Putting Pressure on the USD

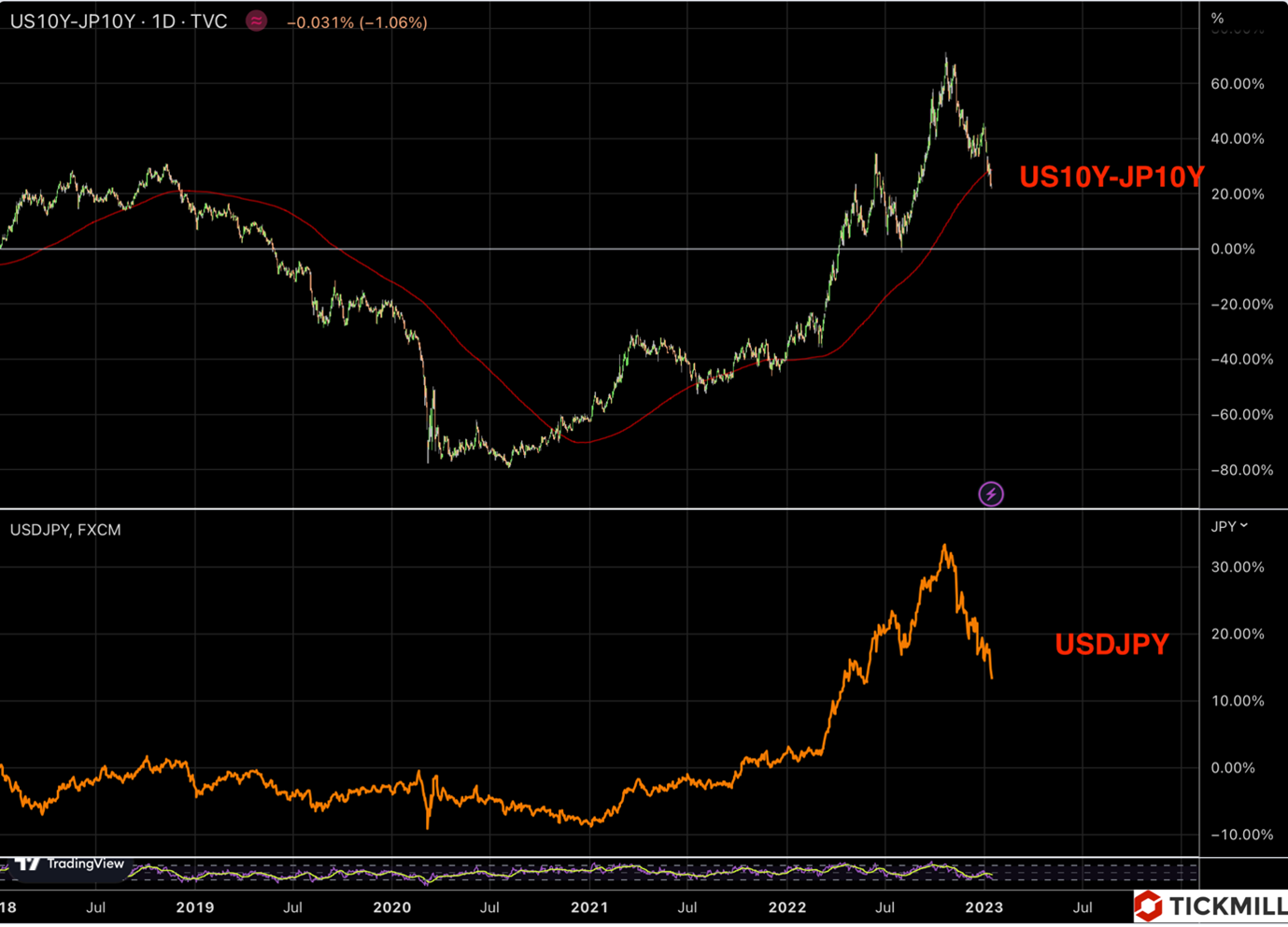

US equities closed in green on Thursday, while on Friday a profit taking mood prevails with US futures on the slippery slope. The dollar index holds above the 102 level, but the yen's strong gains indicate lower expectations that the Treasury-JGB rate differential will remain wide. USDJPY declined 0.75% and closely follows the rate differential:

Despite positive returns in commodity markets today, currencies such as the NZD and AUD are slightly in the red, indicating growing concerns about the economic momentum in China.

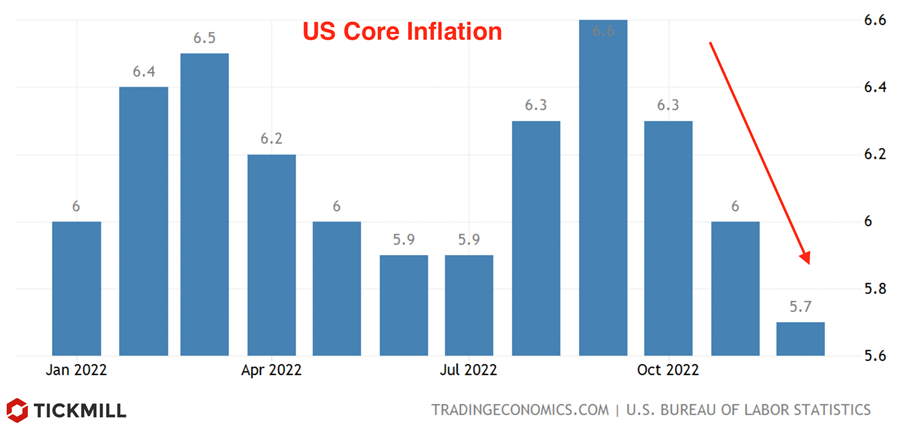

EURUSD tested 1.085 but somewhat erased part of the gains amid an under-hawkish CPI report for December, with the market forecasting less than 50bp. of the Fed tightening in February and March. The 10-year bond yield broke through 3.5% and is trading a few points lower. There is growing consensus in the market that the Fed will raise rates by just 25 basis points in February.

The US December CPI report pointed to lower prices for core goods, but inflation remained strong in the services sector. As a result, the market focus on the labor market data, such as the NFP report, will likely increase as it becomes clear that inflation coming from the services sector wages becomes the key driver of headline inflation:

The February FOMC meeting is getting closer, and the market is divided between whether the central bank will choose a 25basis point or 50 basis point rate hike. After raising rates by 425 bp. there is a strong possibility that the Fed will prefer to fall back to more conventional 25bp increases, given that most of the work on the tightening policy has already been done, and there are signs that the economy is reacting to it. However, inflation remains well above the 2% target and the labor market is still in deficit, with the unemployment rate back to a cyclical low of 3.5%. If the Fed decides to raise rates by 25bp, the regulator will probably try to compensate for such a move by saying that this is not the end of the rate hike cycle and that another 25bp is expected in March. This will leave the Fed funds target range ceiling at 5%.

The flow of data next week will have an important impact on the decision. The calendar includes retail sales, industrial production, housing sales and producer price inflation. Activity is likely to be subdued as retail sales declined due to a significant drop in car sales in December, while lower household incomes and bad weather could also help reduce spending. Industrial production is also likely to fall, given the weakness seen in key surveys such as the ISM report on manufacturing, whose manufacturing component fell into contraction territory (below 50) for the first time since May 2020.

The housing market data is likely to be weak as mortgage rates have more than doubled in the past 12 months, making home buying even less affordable. Given the market fluctuation from excess demand to excess supply, the fall in transactions will also be accompanied by a decline in housing prices.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.