US December CPI in line with estimates, Fed expected to gear down to 25 bp tightening rate

Inflation in the US shows that price pressure is easing, but with strong labor market, the Federal Reserve will be cautious in forecasting the terminal interest rate. The most optimal scenario now looks like two increases, by 25 bp. in February and by 25 b.p. in March. However, inflation will slow even more significantly in 2Q, and the outlook for rate cuts in the second half looks strong as recession risks rise.

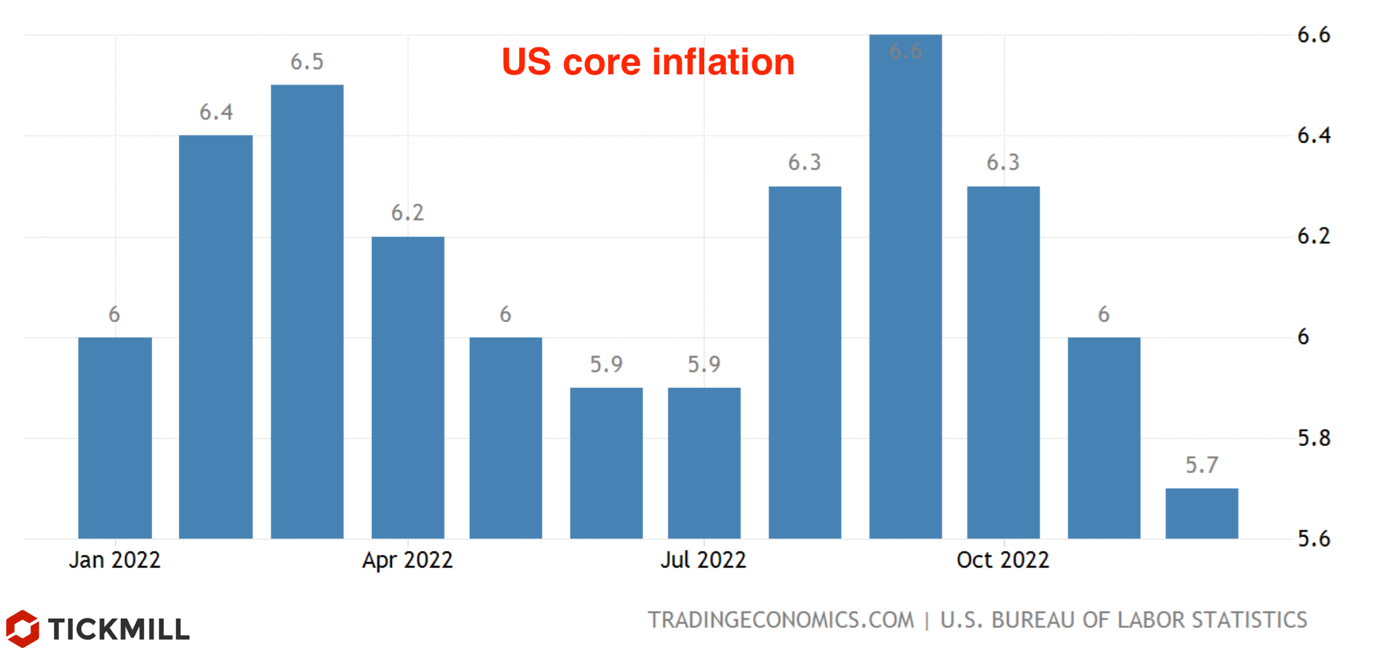

The December US CPI was in line with expectations: -0.1% MoM and 6.5% YoY for the headline index and 0.3% MoM and 5.7% YoY for the core index:

The slowdown continues after the headline peaked at 9.1% year-on-year in June, and the base rate stood at 6.6% year-on-year in September. Inflation is still not below the 0.17% m/m threshold that will lead to the Fed's 2% m/m target inflation over time, but data over the last three months is a notable step down from the average of 0.5- 0.6% m/m observed in the second and third quarters of 2022, which gives the Fed reason to raise rates by 25 basis points from now.

House price inflation remains strong at 0.8% m/m, but with house prices falling in the second half of 2022 and rents now peaking nationally, this will slow rapidly from second quarter of this year. Prices for new (-0.1% m/m) and used cars (2.5%) are falling, and this will intensify in the coming months as demand fluctuates and production continues to rise thanks to improving supply chains. Medical care (+0.1%) will also remain low due to BLS health insurance cost calculations until September, which grew fairly steadily at 0.4-0.8% m/m until 2022.

The Fed insists that key focus should be on services sector given importance of wage costs in a labor market that remains in short supply. The situation looks good here too: airfares are falling, while entertainment rose by only 0.2% m/m, while education/communications rose by 0.1% m/m. Clothing was the strongest component outside of housing, up 0.5%.

So housing appears to be the main issue keeping the core consumer price index above that all-important 0.17% threshold. This is likely to change soon, so the Fed should choose to raise by 25bp. in February - Fed official Pat Harker suggested that such a move "would be appropriate going forward" immediately after publication. However, given the strength of the labor market, officials remain cautious and are likely to hint at a further 25 bps gain in March.

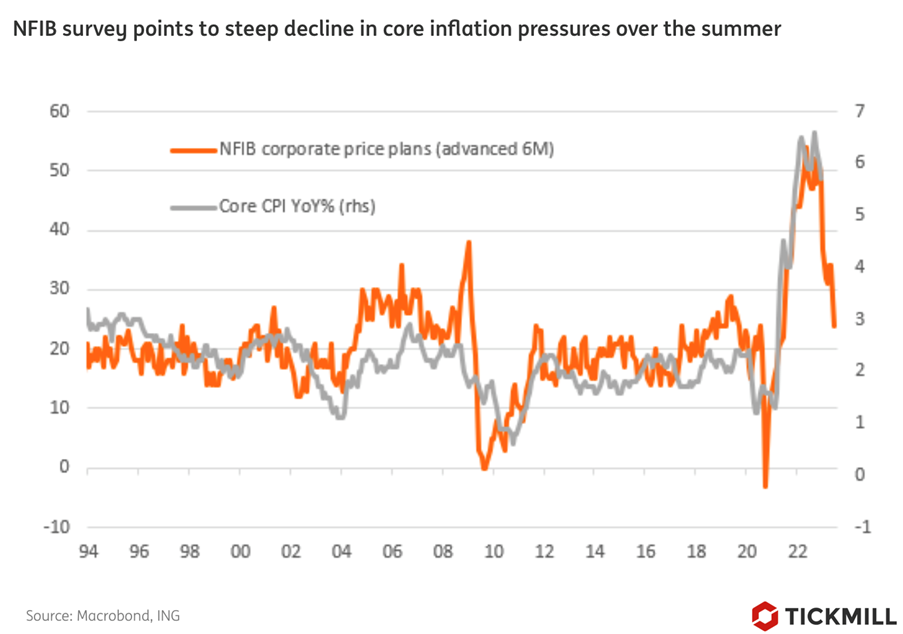

The 5% level is likely to be the highest level for rates, given housing, vehicles, medical care and weak corporate pricing power, which will significantly reduce inflation in the second quarter. As a result, the National Federation of Independent Business is compiling a series of data on the proportion of businesses that expect price increases in the next quarter. It is collapsing as worries about the economy intensify.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.