Weidmann Urges to put off Stimulus, let Lagarde Decide on a new Policy Course

The head of the Bundesbank, Jens Weidmann, said on Tuesday that the ECB did not have to rush to resume easing, as in the current position it would be erroneous to "act for the sake of action." According to him, speculations about the rate cut in September is less and less consistent with the latest news from the economic front.

In general, Weidmann is known for his tough stance against “symptomatic treatment” of the economy’s sore points with credit expansion and the temptations to lower rates in order to accelerate the achievement of inflation targets. In short, Weidmann is a traditional hawk. Only with emergence of the vacant seat of ECB head did he briefly play the role of a pragmatist to compete for the position but lost to Lagarde. At the time of the election, he acknowledged that the ECB's targeted activity on the secondary market of sovereign bonds of Eurozone members in 2012 (Outright Monetary Transactions) was justified for a better transmission of monetary policy, although earlier he had been arguing that such a clear signal of salvation strengthened moral hazard and allowed local governments to relax and put off unpopular reforms.

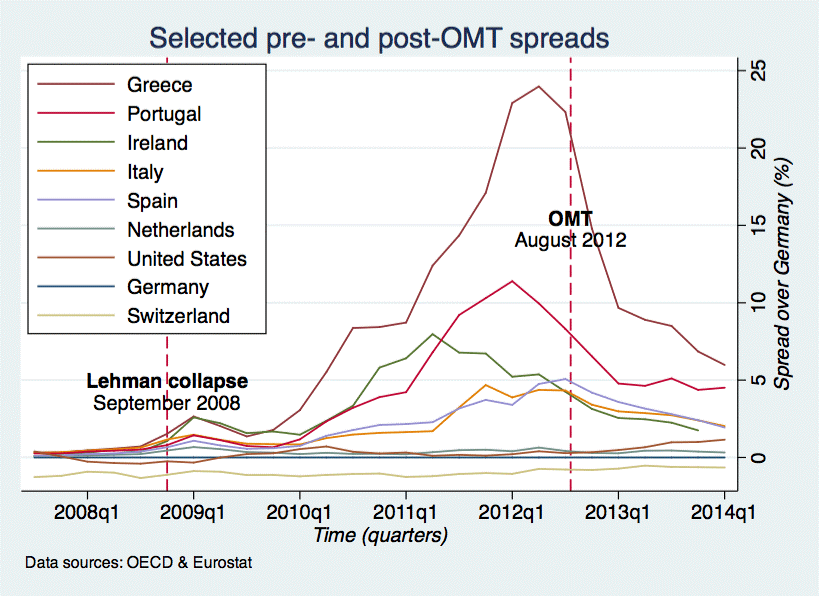

Spread between German bonds and other Eurozone members before and after OMT. We can see how the ECB’s intervention “postponed” concerns related to the credit risk of other members but didn’t solve it.

With Lagarde selected as head of the ECB, Draghi may prefer to refrain from launching a new round of stimulus, which his successor will have to deal with. Not because the economy does not need easing, but because the traditional transmission channel through the interest rate is losing efficiency with rates plunging deeper below 0. In this sense, Weidmann's comments may indicate a gradual transition to a potentially new course in the policy, with emphasis on the fiscal functions of the Central Bank, which I wrote about yesterday. “We need to steer clear from the territory bordering on monetary financing (QE),” Weidmann said.

Weidmann’s permanent opposition to the head of the ECB Draghi, who did not hesitate to scary markets with dovish rhetorics and did not skimp on support measures, forced the latter to call the boss of the German Central Bank the ironic “Doctor No”.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.